This is the abridged version of the article, which can be read in full here.

This was our first trip post COVID to Asia and was a particularly unique trip given the events between visits. It was fantastic to be back on the ground and see whether our regional outlooks/concerns (from an external lens) were valid or overdone, in addition to what regions, sectors and companies looked interesting or concerning. It was a trip that reiterated conviction while also fundamentally changing our view on certain names in our universe. It also reinforced the importance of being on the ground, in-country, and meeting with management teams face to face.

In this piece, we highlight some interesting themes and observations from the trip that supports our ongoing investment in the region.

Politics

The mood on the ground seemed content if not relatively buoyant across the four countries. Domestic politics were not top of mind or raised in conversation, with locals welcoming to foreigners as they moved about enjoying post COVID life. We didn’t feel uncomfortable at any point and would certainly be happy to visit each of the destinations for business or tourism going forward.

Indonesia

Post February’s election outcome, the political situation in Indonesia feels very stable. With a significant majority, the policies of the very successful outgoing president, Joko Widodo, are expected to continue under his nominee, Prabowo Subianto. Subianto is not without a checkered military history. However, domestically he is considered the best option to continue what has been a very stable period in Indonesia’s political history and one which saw strong economic advancements of the middle class.

We are supportive of a continuation of Widodo’s mandate as he has successfully advanced the infrastructure investment in Indonesia in a way that offers investors strong growth and reliable returns.

Malaysia

Politically, Malaysia felt stable. The one recurring concern voiced was around the weakness of the Malaysian Ringgit and potential government directives to limit off-shore flow of capital in support of domestic business and currency.

Some feel that Malaysia could be a beneficiary of the China +1 strategy but to date no strategy seems defined. It is still very early days in determining how they could participate.

Thailand

Thailand is not without a history of political protesting from pro-democracy, criticism of the monarchy, political corruption, up-rising of youth to basic human rights. With the exception of a few, these protests are generally relatively peaceful.

After the Move Forward Party won the 2023 election, but was blocked from forming a government by the military controlled Senate, expectations of protests have been elevated. However, we did not get the impression of any imminent political posturing with a general feel that locals were enjoying the freedom of a post COVID world and benefiting economically from the return of the tourist.

Again, there is some expectation that Thailand could be a beneficiary of the China +1 strategy, but this was also very loosely discussed. We did speak to a private investor in power plants in neighbouring Laos and Vietnam who hoped to capitalise on the regional demand from a China+1 strategy and the associated need for power. It was clear, this investment was not easy and not without political hurdles but the potential return to date had outweighed the cost (time and money) of the associated red tape.

Hong Kong/China

We had expected to see or hear more of the mainland voice in Hong Kong. However, by contrast, the influence felt much more in the background on this trip relative to last (noting that our last trip coincided with the Hong Kong pro-democracy protests of 2019). It definitely felt like Hong Kong is back to status quo as an independent, yet quasi Chinese, territory.

Masks remain very noticeably in force across Hong Kong, including in corporate meetings. This appeared to be by choice, not mandate, noting that culturally Asians were an advocate of the mask even before COVID.

The other point of note is that while historically an ex-pat enclave of Asia, a number of ex-pats have relocated away from Hong Kong post the Covid era and what was considered arduous conditions through the pandemic. This has had an impact on property pricing across the territory. At the same time, increasing numbers of mainland Chinese are now relocating to the territory, taking the position of the departed ex-pats. Would expect a mix of economic and political motivation behind a move to Hong Kong.

Economics

The economic outlook across the region was disparate.

Indonesia, Malaysia and Thailand felt very affordable while Hong Kong was a shock in terms of pricing – this is no doubt partly due to the relative strength of the respective currencies to the AUD (noting the HKD is pegged to the USD).

The economic mood was solid and people in general seemed happy, with many individuals out socialising in shopping centres and bars. Homelessness while prevalent in every major city today, did not feel any better or worse in Asia (noting our time was largely spent in city centres). Public transportation networks were crowded while ride share dominated over taxis in every country.

Indonesia

One thing that's immediately noticeable throughout Jakarta is the extremely congested highways and crowded streets. Novelist Seno Gumira Ajidarma once wrote that ‘the average Jakartan spends 10 years of their life in traffic’, and it doesn’t take long in the Indonesian capital to see why this rings true. Expressways are extremely captive, with many of the 3.5 million people who commute into Jakarta daily travel by car due to the lack of suitable public transportation alternatives.

During the day, most cafes and restaurants were largely empty, likely influenced by the observance of Ramadan. However, the streets were filled with activity. In the evening, the scene shifted dramatically, with many people flocking to street stalls, cafes and restaurants. The atmosphere was vibrant, with activities heard from the hotel well into the evening.

Malaysia

We are always surprised at how developed and advanced Kuala Lumpar feels relative to its neighbouring Asian capitals. The roads are high quality and free flowing, cars were relatively new and mopeds/bikes were in limited use, the shopping areas were full of western brands and the city centre real estate was on par with a developed capital.

Unfortunately, we visited in the middle of Ramadan so the feel on the ground was probably a little quieter than normal. However, the general mood of the locals we met appeared very content and as always incredibly welcoming to foreigners.

As noted above the Malaysian Ringgit has been notably weak which is partly also why Kuala Lumpar felt very affordable, if not cheap, as a westerner visiting.

One other data point deserving of comment was the rise of Grab (Asia’s equivalent of Uber) which while very convenient and comfortable was also in very high demand throughout the day with wait times of 15 minutes or more for a ride in peak periods.

Thailand

The COVID shutdowns hit the heavily tourism dependent Thai economy hard, compounded by a slower post COVID economic rebound relative to its ASEAN peers. Knowing that, interestingly it felt like the buzz of Bangkok was well and truly back to pre-Covid times. With huge traffic congestion, crowded metro systems, bustling tourists filling the streets and restaurants, and locals actively engaging with the vibrant restaurant scene, the city was alive and bustling.

This tourism recovery has been bolstered by a pickup in arrivals from China and Malaysia this year as well as the implementation in September 2023 of a visa-free policy for visitors from China and Kazakhstan. Like Malaysia, Bangkok offered incredible affordability in local areas. However, in tourism centres, while it remained relatively affordable, there was certainly a premium that tourists were happy to pay. This is no doubt in part due to much lower inflation relative to regional and global peers helping to keep pricing down. For example, a lunch at a local Thai restaurant, with queues of locals waiting for a seat, set us back a huge A$8 for two rice dishes and cans of soft drinks. By contrast a single drink in a tourist bar set you back A$11.

From an infrastructure versus economics standpoint, there were a couple of interesting points:

- The road network was highly congested and slow moving. Even the expressway network was very busy at times. Interestingly, on the expressway network, the majority of toll payments still seemed to be cash by choice – automatic tolling was available but every transaction we had was via the cash channels and this included taxis and Grabs.

- The metro system which was still relatively new on our last visit has been significantly developed. Importantly, it is widely used, air conditioned, comfortable and very affordable. They were standing room only on every line we used.

Hong Kong

A tail of two cities

- Hong Kong island was very lively – people on the streets and in the restaurants and bars. This may be due to arriving at the end of the Rugby Sevens which does see an influx of tourists, but in general it felt like the Island was returning to normal post COVID with very few vacant areas.

- By contrast, Kowloon felt flat. Many of the shop fronts were vacant and the streets felt quieter. It feels like this ‘local’ side has been harder hit and will take longer to recover.

Universally however, things felt very expensive. Our tour of the supermarket found eggs by the dozen at A$25 (Australian equivalent A$12.95), Lurpak butter at A$19.50 (A$5.80), Nutella at A$11 (A$6.85), steak at A$90 kilo (A$40). However, discussing this with one management team, our supermarket study is probably overstating prices, as locals only use supermarkets for pantry items and imported goods, with all fresh produce, meat and dairy purchased at the wet markets where pricing was much more reasonable.

Restaurants and shopping centres were also quite expensive when comparing to their Asian peers, but also relative to Australian pricing. However, despite the increased pricing, restaurants remained full, and locals had no problems paying A$9 for a very mediocre cup of coffee.

Interestingly, there has been a complete 180 on the relative attractiveness of Hong Kong shopping versus the mainland. Historically, mainland residents used to make the trip to Hong Kong just to shop and now Hong Kong residents are spending their weekends on the mainland for the same purpose with luxury and household shopping being much more affordable in RMB versus HKD.

Moving around Hong Kong proved very easy with Uber’s abundant and generally a Tesla!

China

Mainland concerns around the property sector dominated. However, interestingly, everyone we spoke to felt that the Chinese property situation would resolve. It would not be immediate, but they felt in the next few years (2-3) the situation would normalise. Importantly, it became very clear, that there is a significant disconnect with Tier 1 cities, where property demand remained buoyant versus Tier 2 and 3 cities where the situation remained untenable. For example, a property development in Shenzhen city saw all but six units (out of ~200) pre-sold on day one of pre-sale opening. By contrast books of inventory in Tier 2 cities were not moving.

The other prevalent theme, discussed further below, is the increasing dependence of mainland investors on corporate dividend yields. With historical investment in the property sector out of favour and interest rates moving down, mainland investors are looking to the equity markets for a secure form of return, through yield. This is providing downside support to strong dividend payers but also seeing companies that cut their dividends immediately punished. This was very evident in the fiscal year reporting season where a dividend disappointment, no matter how big or small and irrespective of other metrics and fundamentals, saw stocks sold off anywhere from 5-20% on the day. Importantly, the strong management teams are cognisant of the importance of a stable, growing dividend while weaker management teams seemed to ignore these investor concerns/requirements to their detriment.

Infrastructure

While much is happening across the Asian infrastructure landscape, this trip really highlighted and reinforced some strong thematics including:

- Passenger travel: Despite global affordability issues, travel momentum remains strong, even with a slower Chinese recovery. This appears to be partly structural, but even if not, we see positive ongoing passenger and earnings momentum through at least 2024 which we continue to capitalise on.

- Ports: Volumes certainly reflective of the softening of global demand and increased geopolitical conflict but Asian players are well positioned and attractively valued, albeit with absence of near-term organic catalysts.

- Energy: The Energy Transition is a theme in the emerging world just as it is in the developed world with significant discussion on how corporates can capitalise on it, the shift from coal to gas, how waste to energy can play a part, long term investment requirements and who pays for it. These discussions included M&A opportunities versus organic growth potential as well as the impact of recent falls in commodity prices.

- Communications: The rise of data is another global infrastructure thematic. Who, how and when this theme can be captured was an interesting discussion.

- Management strength: A key takeaway from this trip was the relative strength of various management teams – those capitalising on the opportunities afforded to them whilst cognisant of investor concerns/demands, versus those that seemed to execute without consideration of shareholder interests. This theme saw us exit positions while reinforcing commitment to others.

We touch on each of these below, as well as wrap up a few other sector dynamics.

Airports

Traffic recovery supported by policy and demand

The global air passenger traffic volume in 2023 was at 94% of 2019 levels, with domestic traffic at 104% and international traffic at 88% of pre-pandemic levels1. The Asia-Pacific region continued to lag with the overall recovery rate at 86%, with domestic at 102% and international at 73%. While there has been a swift rebound in domestic tourism, international tourism was tepid largely due to the notable absence of Chinese tourists. Unsurprisingly, Chinese outbound tourism had been weak given the country’s complicated and delayed reopening, weak consumer spending, lengthy visa and passport processing times, and reduced airline capacity.

However, in 2024, China's outbound tourism sector has seen a resurgence. Projections from Dragon Trail International2 suggest that China’s outbound tourism is expected to reach approximately 80% of pre-pandemic levels by the end of this year (compared with 48%3 in 2023), with a full return to pre-pandemic levels expected by the end of 2025. Ongoing post-pandemic traffic momentum was confirmed by management teams. Malaysia Airports (MAHB) expects monthly international passenger traffic recovery to exceed 90% in the first half of 2024, ultimately surpassing 2019 levels by the end of the year. Similarly, Airports of Thailand (AOT) are guiding for total passenger traffic across its network to recover to 85% in 2024 and exceed pre-pandemic levels by mid to late 2025.

Visa-free initiatives introduced in recent months have significantly contributed to the recovery in China’s outbound tourism. Most Chinese tourists are traveling to ASEAN countries, with the top destinations including Thailand, Singapore, Malaysia, Vietnam, and Indonesia. Additionally, Asian markets currency devaluation has played a large role in determining travel tendencies. Outside of ASEAN, popular destinations are the United States, the United Kingdom, South Korea, Japan, and Australia. This resurgence of Chinese tourism is expected to further boost international passenger traffic in the Asia-Pacific region and globally, accelerating the recovery of the broader tourism and aviation sectors.

Passenger recovery to support non-aeronautical earnings

During the pandemic, non-aeronautical revenues were negatively affected due to muted passenger throughput and abatements or incentives offered to retail partners. For example, AOT renegotiated the minimum rental guarantees with its duty-free concessionaire, King Power, in exchange for a higher revenue share. Likewise, MAHB waived the minimum guaranteed payment requirements to support retail tenants. Importantly, non-aeronautical spend (retail, food & beverage, and services) has correlated with the resurgence in passenger recovery and also benefited from the removal of abatements. Retail utilisation levels have increased from pandemic lows to in excess of 85%. Management teams anticipate this trend to continue towards the long-term optimal utilisation level of approximately 95%.

Historically, the average spend per basket of goods in Malaysia was around RM230, but since COVID this has increased to approximately RM330. Management highlighted that the changing product mix has been a key driver of this growth, along with higher inflation, which has also contributed to the increase in headline sales. AOT have minimum revenue guarantees with King Power, ranging from Bt7 to Bt233 per international passenger, depending on the airport. The collective revenue per international passenger across AOT's portfolio peaked at Bt218 before the pandemic. When passenger spending exceeds the minimum guarantee at each airport, AOT is entitled to a revenue share. To boost revenue, AOT is working closely with King Power to improve spending by diversifying product offerings and exploring strategies to convert terminal dwell times into spend. AOT noted the increasing preference among travellers for local and specialty stores over traditional big brand names and luxury goods.

The shift in demand towards local and speciality stores over traditional big brand names and luxury goods was evident in the Suvarnabhumi Airport (BKK) departure terminal.

The recovery in Chinese tourism is also set to significantly boost non-aeronautical revenues, as Chinese tourists notoriously rank among the highest travel spenders globally. According to UN Tourism statistics, Chinese tourists spent US$133.8 billion on outbound tourism in 2019, with a per capita consumption of US$863, ranking first in the world for outbound tourism expenditure and representing 23.8% of the global total. The potential for ongoing growth in Chinese outbound tourism is substantial, with the World Travel Market Global Travel forecasting that the value of China's outbound tourism will increase by 131% from 2024 to 2033. While in Europe, we have seen evidence of a pullback in Chinese spending this does not appear to be the case across Asia so far.

Regulation

MAHB has experienced a re-rating following the continued momentum behind its transition to a regulatory model. The recently signed Operating Agreement (18th March 2024) not only extends the airport network concession term by 35 years to 2069, but signifies a more comprehensive and dynamic approach to pricing mechanisms and investment.

Starting from Regulatory Period 2 (RP2) in 2027, Passenger Service Charges (PSC) will be determined using a building block model, moving away from the previous system of inflation indexation every five years. This new approach considers various factors such as operating costs, market demands, and broader industry dynamics, enabling a more comprehensive and dynamic pricing structure. The building block model allows for a more nuanced calculation of PSC, reflecting the actual costs and needs of operating an airport network. This includes considerations like capital expenditures for infrastructure development, operational expenses, and expected returns on investment. The flexibility inherent in this model provides MAHB with greater scope to adjust to changing market conditions, ensuring that the PSC accurately reflects the airport's financial requirements and economic environment. Management believes the company is currently under-earning compared to regulatory input methodologies and anticipates a material step-up in PSC charges under the framework.

AOT last raised passenger service charges in 2007, resulting in a 40% uptick to international passenger charges and a 50% increase to domestic charges. In 2013, AOT sought a further increase of 14% for international passengers, and a 50% increase for domestic passengers but this request was rejected by the Department of Civil Aviation (DCA). AOT plans to commence a further study on passenger service charges this year and are in the process of hiring an external consultant to assist. Management anticipates the study will take at least 12 months and will determine the quantum of increase to be sought. Once the study is completed, AOT will submit the findings to Civil Aviation Authority of Thailand (CAAT) and the Ministry of Transport (MOT). After their review, a formal submission will be made to the Cabinet for final approval. The entire process is expected to take at least 2-3 years, with no guarantee of a price increase, which is disappointing.

A key concern for AOT is the government's proposal to abolish duty-free on arrival. The proposal is still under consideration, with feedback being gathered from stakeholders like AOT, King Power, and the Ministry of Finance. Duty-free on arrival accounts for less than 10% of gross floor area (GFA) and less than 10% of concession revenues. AOT believes the move will not yield the desired effect of encouraging foreign tourists and returning Thai travellers to make more in-country purchases. They suggest that most passengers, whether foreign or Thai, tend to plan ahead and would duty-free shop on departure. While King Power, the duty-free concessionaire, could repurpose the floor space with different commercial activities, AOT anticipates that removing duty-free on arrival would lower revenue per passenger, affecting contractual obligations. If the policy proceeds, AOT might have to reduce the minimum guarantee per passenger, but this could be partially offset by higher revenue share arrangements.

M&A

MAHB has been the subject of potential takeover speculation following an article4 published in The Edge Malaysia Weekly on the 24th of February, 2024. The article suggests that the company’s major shareholders Khazanah Nasional (33.24%) and Employees Provident Fund (6.07%) are looking to formulate a strategic partnership with Global Infrastructure Partners (GIP) to operate Malaysia Airports. The article does not specify whether this partnership would involve equity participation from GIP, a secondary placement of shares from Khazanah & EPF to GIP or a consortium-led privatisation. Given the airport network would be considered national assets, a 51% holding by government and/or domestic nationals would be required.

We do not see the timing of news as coincidental given MAHB's transition to a regulatory model and its strong underlying value. According to FactSet consensus data, MAHB remains one of the most attractively valued listed airports, with a forward EV/EBITDA of 7.5x compared to the sector average of 11x. GIP, with its extensive experience in global airport management, could help to improve operations and bring significant financial capacity, supporting the funding requirements for Malaysia's extensive airport network.

Potential corporate actions present upside risk, but does not underpin our core investment thesis. We find MAHB offering solid value at current prices, with ongoing passenger recovery and a shift toward higher-yielding international traffic to drive earnings and distribution growth.

Utilities

Chinese gas utilities

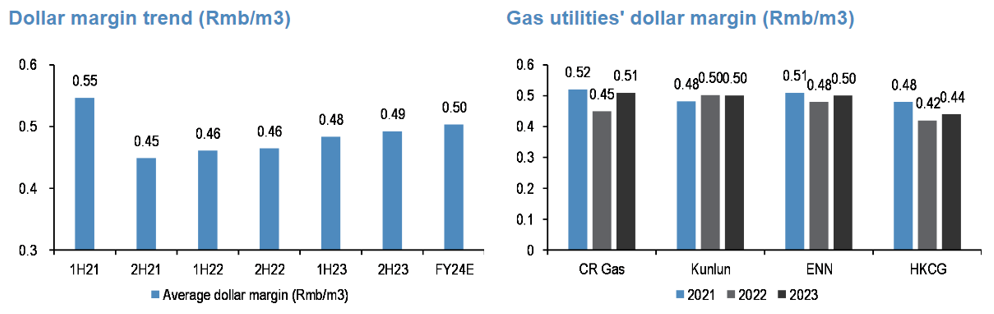

The market has always been focused on the sector tripod, being; (i) gas sales volumes growth, (ii) dollar margin, and (iii) new connections.

Source: Company

*China Gas Holdings (CGH) excluded. Not comparable due to its fiscal year ending 31 March, nor has the Company provided any FY25 guidance to-date

-

Gas volumes: 2023 gas volumes fell flat after a reopening that never materialised, causing operators to revise their guidance downward or predict declines in volume. For 2024, city-gate operators remain somewhat cautious, providing volume growth guidance ranging from 5-10%. This reflects a conservative outlook amid market uncertainties. Among the major city-gate operators, ENN Energy (ENN) is expected to benefit from an increase in gas volume from high-end manufacturing and renewable sectors, while China Resource Gas (CR Gas), TownGas China (HKCG), and China Gas Holdings (CGH) foresee robust commercial demand and growing household consumption. Despite the short-term uncertainty, management believe the long-term prospects for robust gas demand growth remain intact. This is underpinned by continuous recovery in macroeconomic conditions, China's dual carbon policy, ongoing industrial coal-to-gas conversion, industrial upgrades, and increased urbanisation. The Central Government projects that domestic gas demand will reach approximately 600-700 billion cubic meters (bcm) by 2030, up from around 395 bcm at present. This projection implies a compound annual growth rate (CAGR) of 6-9% over the coming years. Given this outlook, city-gate gas operators have set goals to maintain volume growth at or above the industry average and we got comfort from conversations thereon with messaging similar across the sector.

-

Dollar margins5: High global gas prices, combined with constraints on passing through procurement costs to residential customers, have resulted in dollar margins for city-gate gas operators being squeezed. Margins have dropped from the previous levels of RMB0.55-0.60 per cubic meter (cbm) to RMB0.45-0.50/cbm in 2023. However, ongoing policy reforms aim to address this issue by creating a framework that allows a more direct and timelier pass-through of increased costs to residential customers. Going forward, many operators anticipate sequential improvements and for dollar margins to stabilise at a normalised level of around RMB0~0.55cbm, depending on the customer mix. The exact margin will depend on factors such as the ratio of residential to commercial and industrial customers, the degree of pass-through allowed, and other cost control measures.

Source: Companies’ Results Presentation (FY/Interim 2021-23), J.P. Morgan calculations. Note: Average of CR Gas, ENN, HKCG, Kunlun -

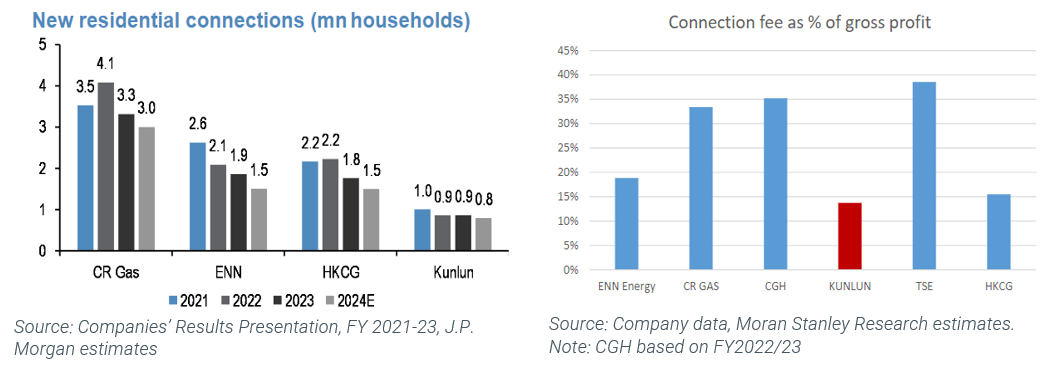

Connections: Connections, both for new and existing dwellings, have historically been the priority of the sector given the segment’s superior margins. The recent downturn in China's property market weighed on connections, as new connections in general contracted by 10-20% in FY23, reducing the segment's contribution to overall earnings. In 2024, new connections remain modest, with gas names guiding flat to 20% YoY declines, but positively benefiting from improving margins. Most operators expect to maintain a steady level of connections in the next few years, before a gradual decline thereafter. Even prior to the recent property market woes, our forecasts indicated a similar trend; the current circumstances have merely accelerated the timeline. Additionally, we do not model additional concession wins, only increased household penetration with the incumbent operating footprint.

Management teams were unified in their strategic focus on maximising value from incumbent operations rather than aggressively pursuing new concessions. This shift in approach underscores the significant potential for growth and profitability by enhancing current assets and expanding services within existing operations. By leveraging existing customer relationships and infrastructure, they can maximise value of their assets and open new revenue streams. We think this is an important and much needed sector transition. Key strategies include:

- Increasing customer penetration: Targeting higher penetration rates among both residential and commercial & industrial (C&I) customers in existing jurisdictions offers a way to grow revenue without the need for extensive new infrastructure. This can involve outreach efforts, promotional activities, and incentive programs.

- Increasing usage per customer: Encouraging existing customers to increase their gas usage can be achieved through targeted marketing, discounts, and providing solutions that meet specific customer needs. By understanding customer behaviours and preferences, operators can design campaigns that stimulate demand.

- Expanding dollar margins: The pass-through framework allows operators to adjust prices in response to cost changes, providing an opportunity to maintain or improve dollar margins. Additionally, exploring operational efficiencies and cost-reduction measures can further contribute to profitability.

- Offering Integrated Energy (IE) and Value-Added Services (VAS): These services encompass a wide range of activities, from energy management and equipment maintenance to broader energy consulting services. By expanding these offerings, operators can diversify their revenue sources and strengthen customer relationships. Some operators believe that the earnings contribution from these activities could eventually rival that of their core gas sales business.

Thai electricity utilities

The Thai electric utilities typically operate across three segments. Independent Power Producer (IPP), Small Power Producer (SPP), and/or Very Small Power Producer (VSPP).

In the latter half of 2023, utilities with large SPP portfolio exposure de-rated due to the Energy Regulatory Commission (ERC) freezing the energy tariff adjustment and concerns of potential incremental tariff cuts (having lowered the band of electricity tariffs by ~10% for the May – August 2023 period). This action, intended to lower energy costs and stimulate the Thai economy, led to margin squeezes as rising procurement costs could not be passed on to end-users. Regulatory focus on consumers came at the expense of the operators. Consequently, the Energy Generating Authority of Thailand (EGAT), a state-owned agency and the largest power producer and wholesaler in Thailand, incurred an additional ~Bt110bn in debt, putting its credit ratings in jeopardy. The sector has seen some reprieve through declining prices (gas and coal), along with a recent ~5% upward tariff revision in January 2024. Whilst declining gas and coal prices aid in margin expansion, the utilities are unlikely to retain this benefit for long given the Move Forward Party’s emphasis on energy policy measures, which could see a tariff cut follow to reflect the declining procurement costs. Some utilities are attempting to expedite the margin recovery through portfolio optimising and contract structures, particularly by increasing gas-linked tariffs with industrial customers. The failure of the regulatory construct/contract structure with little judicial recourse has long been a concern for us with the sector, and a reason we are not invested despite the opportunity underpinned by the country’s evolution.

Thailand’s latest iteration of its Power Development Plan (PDP, 2020) has set a net zero greenhouse gas emissions target for 2065 and carbon neutrality for 2050. Whilst this underpins the need for new renewable capacity over the long-term, the SPP and IPP markets are presently oversupplied and many of the utilities are uncertain as to whether they can successfully renew/replace capacity as contracts expire. This has increased the competition in domestic renewable energy bidding processes and pushed utilities to seek opportunities abroad to supplement growth and insulate from potential non-renewals of capacity. GPSC highlighted its ongoing investment in Avaada Energy Private Limited (AEPL), a renewables platform in India, and an offshore windfarm in Taiwan. BGRIM plans to pursue new greenfield and brownfield projects in countries such as Malaysia, Philippines, Cambodia, Vietnam, South Korea and Japan. BGRIM are currently constructing the Nakwol 1&2 offshore wind projects in South Korea which have a combined capacity of 740 MW (363 Mwe). Whilst these overseas investments signify a strategic shift, the utilities remain focused within the energy sector, with strict investment criteria requiring ’double-digit’ equity IRR returns.

Despite these near-term challenges, the utilities are optimistic about electricity demand in Thailand, expecting a sustained annual growth rate of 3-5%.

Ports

Maritime trade outlook

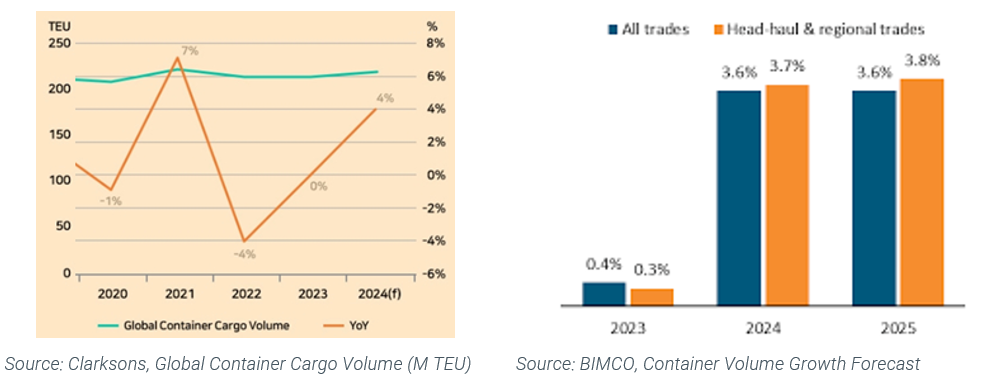

In 2023, the container market grew a modest 0.2%. Compared to 2019, before the pandemic, the market has seen an overall growth of 1.5%. Despite fluctuations in various economic indicators, global container volume growth has shown resilience. According to data from BIMCO and Clarksons, global container volume is forecast to grow by 3-4% in 2024, while Maritime Strategies International predicts a slightly more optimistic growth rate of 4.5%.

Port operators in the region had a similar outlook, but alluded to upside-risk. China Merchants Port (CMP) recorded a 10% increase in container throughput across its global terminal network for the first two months of 2024 but affirmed ‘flattish’ full-year growth guidance due to a low base effect in the first half and a cautious outlook for the latter half of the year. Specifically, they expect domestic throughput growth of 1-2% and throughput at its overseas terminals to grow slightly higher at 2-3%. COSCO Shipping Ports (COSCO) are slightly more optimistic, guiding to ‘mid-single digit’ growth. Westports (WPRTS), a key transshipment port located along the Asia-Europe and intra-Asian shipping lanes within the Strait of Malacca, has guided for ‘low single-digit’ container volume growth. Longer-term, they expect container volume growth to stabilize around 2-3% per annum suggesting limited organic growth opportunities.

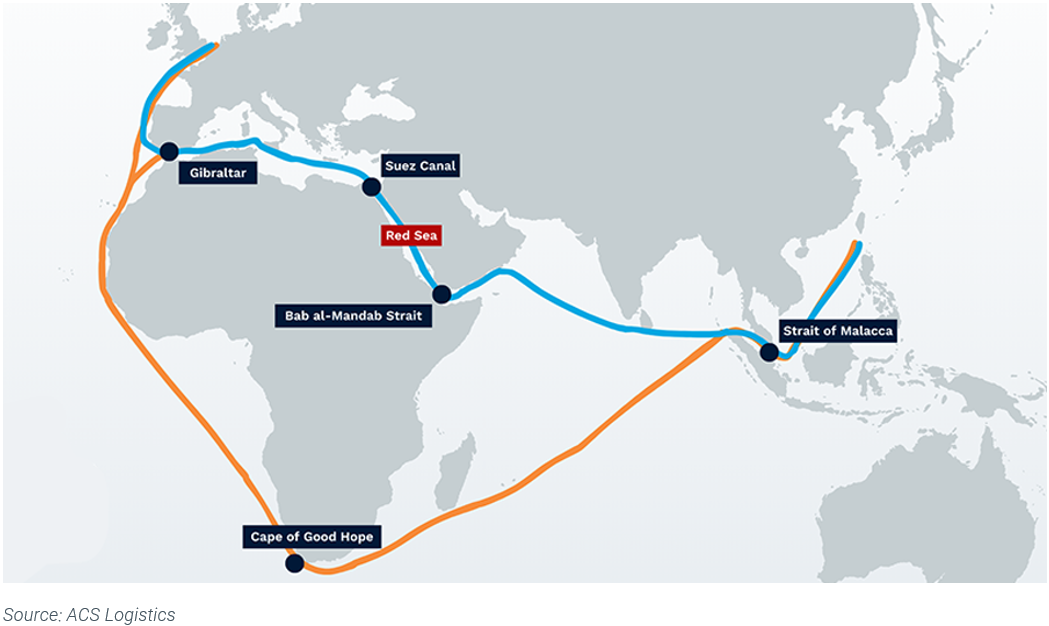

The Red Sea disruptions

Attacks on vessels in the Red Sea area have significantly disrupted traffic through the Suez Canal, the shortest maritime route between Asia and Europe and responsible for about 15% of global maritime trade volume. According to UN Global Platform and IMF PortWatch, trade through the Suez Canal in the first two months of 2024 dropped by 50% compared to the same period in 2023. Shippers have chosen to avoid the Suez Canal and reroute via the longer Cape of Good Hope, extending journey times by more than a week and adding over 3,500 nautical miles (6,500 kilometres) to their voyages. UBS estimates that this re-routing translates into a 20-30% increase in cost per container.

Port operators indicated that ocean carriers' networks are settling into a ‘new normal’. Despite the logistical challenges, they indicated that even if Suez Canal diversions persist, apart from longer voyage times, the frequency of ship calls are expected to be sustained.

Supply chain shifts

Supply chain shifts aren't new. They've been ongoing and driven by a range of factors including diversification, cost-cutting, tariffs, subsidies, geopolitical risk, lead times, and ESG considerations. The supply shock that started in China during the pandemic and the demand shock that followed only emphasised and accelerated efforts to reduce vulnerabilities in production strategies and supply chains. Companies are increasingly re-evaluating their approaches to address these risks and enhance resilience, focusing on regionalisation, reshoring, and multi-sourcing to create more robust and flexible supply networks.

CMP and COSCO have taken steps to mitigate risks associated with changing global trade dynamics by investing in global terminal networks. This approach allows them to capture shifting trade flows amid ongoing supply chain realignment. Both companies have expressed concerns about industrial migration and the ‘China +1’ strategy, which involves companies diversifying their manufacturing bases outside China. However, they are also looking to capitalise on these trends by investing in new terminals in regions expected to benefit from this shift. CMP and COSCO believe that the domestic impact of these changes can be mitigated by the Central Government's mandate on boosting high-end industrial goods production, allowing China to remain competitive while adapting to global supply chain shifts.

Port charges

Through and post the pandemic, container capacity shortages, terminal congestion, and global inflation combined to elevate shipping rates, boosting shippers’ profitability. These favourable conditions enabled most terminal operators to negotiate higher port charges. Shipping rates have since normalised, and further pressure is anticipated as global GDP decelerates and additional shipping capacity comes online, which could impact shipping profitability. This outlook could see terminal operators face greater resistance for future fee hikes.

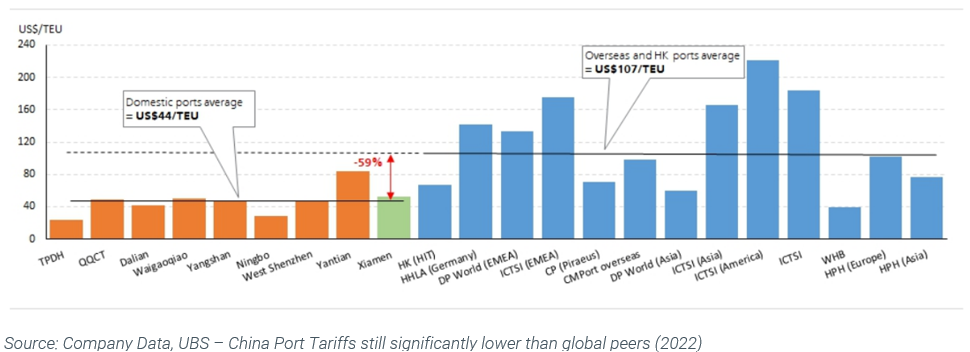

CMP and COSCO management expect benign tariff increases at domestic terminals of 1-2%, while aiming to implement inflation-like tariff increases at overseas terminals. Longer-term, we see a strong case for future tariff hikes at mainland China ports given the pricing disparity with global peers. Average revenue/TEU at mainland China ports in 2022 was US$44/TEU, while international ports were US$109/TEU. Notably, we do not factor domestic tariff increases into our assumptions, thus representing upside risk.

Westports, on the other hand, operates under a different model. While the company negotiates directly with shippers, the Port Klang Authority sets maximum ceiling rates. WPRTS has commenced the process of requesting a container tariff revision, aiming for increases similar to the last review in 2019 (+30% for transshipment, +20% for Origin & Destination). The process is expected to take 1-2 years to complete and implement.

Expressway operators

Traffic

Expressway traffic in China has rebounded significantly post pandemic. According to data from the Ministry of Transport (MOT) and UBS, expressway traffic was estimated to have increased by 34% in 2023. Although we anticipate growth to be moderate in 2024, expressway operators are still expected to see continued traffic volume growth, driven by ongoing economic recovery, strong domestic travel demand, resilient freight activity and structural shifts in travel modes.

Jasa Marga (JSMR) were upbeat on traffic growth in 2024, guiding for a 5% increase in traffic and a 10% increase in revenue. Management expects traffic growth to remain above 5-6%, supported by the ramp-up of new and recently commissioned expressways. Within its diverse portfolio of 36 toll road concessions, JSMR reported that only three are underperforming compared to expectations. For two of these underperforming concessions, the primary reason for the shortfall has been underinvestment by the government in the surrounding infrastructure and economy, which had been promised when the concession deeds were formulated. Given that the government's commitment to deliver the necessary investment was part of the concession agreements, JSMR is allowed compensation, with negotiations currently underway and showing progress.

Unlike its expressway operator counterparts in China and Indonesia, Bangkok Expressway and Metro (BEM) in Thailand has observed clear structural shifts impacting traffic. These shifts include work-from-home (WFH) practices, changing lifestyles, the opening of competing routes, and greater integration with the metro network. As a result, expressway traffic recovery has stalled at about 90% of pre-COVID levels. With expected traffic growth of 2-3% per annum, it may take several years to exceed pre-pandemic levels.

Tolls

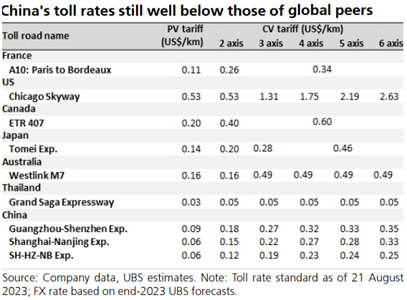

Unlike most toll roads elsewhere in the world, toll rates in China have not been a major growth driver as they are not automatically increased in line with inflation or other return-based indexes. While concession contracts include provisions for requesting toll rate increases, these provisions have not been utilised owing to the superior traffic volume growth observed. Consequently, toll rates in China are substantially lower than in many other countries. Recent policy discussions reference improving the flexibility in setting and adjusting toll rates as a means to enhance and ensure sector returns.

Toll rates on BEM’s Expressway Sectors jump every 5-10 years. Although this results in one-off increments of 15-20%, the smoothed effect over the decade is approximately 3% per annum, providing a slight cushion above the national inflation rate.

Development opportunity set

Having experienced a period of limited greenfield development in several provinces, numerous expressway operators in China leveraged the stable cash flow from their existing expressway businesses to invest in alternative ventures. Whilst these investments have typically yielded incremental earnings, a number of these would not be considered traditional 'infrastructure'. Positively, despite these investments, the expressway businesses have always remained the major composition of earnings, ranging from 75% to 100% with 4D Infrastructure favouring those operators maintaining an infrastructure focus. In recent years there has been a noticeable shift back to focusing on core expressway operations, a move we view as positive.

Several key expressways in China are nearing the end of their concession periods and require redevelopment and expansion (R&E) to address and alleviate increasing congestion. Expressway operators have commenced, or are in preliminary discussions, with the respective provincial governments to advance various R&E plans. These projects are expected to deliver incremental returns and extend the average concession periods for the operator’s expressway network. Management teams confirmed positive momentum on these discussions, yet we do not factor these renewals/extensions into valuations until signed.

JSMR has been investing heavily in the network for years and while there has been a slowing in greenfield momentum, they still have direct or indirect ownership in five new toll road developments, each to be constructed in sections. The total estimated cost of these projects is expected to exceed IDR85 trillion, with JSMR's share amounting to approximately IDR60 trillion. Developing in sections suits the company as it aims to manage its balance sheet and maintain a positive free cash flow profile. All development projects are expected to meet or exceed JSMR's internal return hurdle of 13%. If a project fails to meet these expectations, the company can seek adequate remuneration to ensure it is made whole. Additional opportunities may be sought through tender, acquisition or unsolicited proposals.

BEM is actively exploring one major expressway development, the Bt35 billion FES Double Deck Project. This project is still in the preliminary stages, with the Environmental Impact Assessment (EIA) recently completed. For the project to be viable, an extension of the FES concession, currently set to expire in 2035, will be required. Construction is expected to take 4-5 years, with the extended timeline aimed at minimising traffic disruptions. BEM plans to focus most of the construction work during nighttime and off-peak hours to reduce the impact on daytime traffic.

Regulation, contract & policy

Policy support is expected to be instrumental in driving a re-rating of the expressway sector and reigniting an investment cycle for existing, mature expressway assets in China. The sector has experienced a de-rating following government interventions, both central and provincial, that has hindered overall revenue quality without providing adequate compensation. Measures such as toll cuts, toll-free periods, and toll discounts have been implemented, alongside the absence of a clear cost-based tariff setting or capex-recovery mechanism. Policy support started gaining traction in 2023 when the Ministry of Transport (MOT) pushed for the finalisation of the 'Toll Road Management Ordinance' within the 14th Five-Year Period (FYP, 2021-2025). This Ordinance, first drafted in 2015, aims to overhaul the expressway sector's return profile by considering cost and capex factors and allowing adjustments to concession tenor and toll rates to ensure adequate returns. Provincial rules for pricing mechanisms in expressway expansion has been flagged for review within the 15th FYP (2026-2030).

We are optimistic about the supportive policies for the toll-road sector for two main reasons:

- Expiring concession periods: Several major expressways in China are nearing the end of their concession periods and require a robust framework to ensure adequate returns from any potential investment in redevelopment and expansion.

- Provincial government financial strain: Provincial government-owned expressways are experiencing financial strain, with some provinces unable to afford interest payments on their obligations.

Multiple expressways run by listed operators are heavily congested, necessitating R&E to facilitate smoother traffic flow. With limited tenor remaining on the concession periods (5-10 years), the operators have been reluctant to invest in costly expansions. However, following the Central Government's guidance to implement more favourable policies for toll road projects to ensure reasonable returns (i.e., lifting the concession period cap from 25 to 30-40 years), all the listed expressway operators have initiated dialogue with the respective local governments to advance R&E. Additionally, the operators aim to leverage special-purpose local government bonds to lower interest cost and enhance returns.

Supportive policies are essential to ease cash-flow pressures for local governments and help fund significant capex requirements for expressway expansion in the future.

Communications

Indonesian towers

New tower builds in Indonesia had stalled following the 2022 merger of mobile network operators (MNOs) Indosat Ooredoo and Hutchison 3, forming Indosat Ooredoo Hutchison (IOH). While MNO consolidation generally supports long-term industry fundamentals, including financial stability and investment planning, it can also cause short-term disruptions. The stall in new tower builds occurred as IOH undertook tower network rationalisation, aiming to reduce overlapping sites by renegotiating with the TowerCo’s to reallocate equipment to new sites or allowing leases to lapse. Furthermore, other MNO’s remained relatively idle, adopting a ‘wait and see’ approach to determine IOH's new strategic directive. Positively, the order book has started to pick up.

Indonesian TowerCos see multiple growth opportunities in the sector, driven by data consumption growth, further investment requirements in 4G networks, and the anticipated build-out of 5G. On 4G, despite the high network population coverage of over 95% and improved availability rates (the average proportion of time users spend connected to 4G on each operator's network), the existing 4G infrastructure suffers from inadequate capacity. While all operators surpassed the 90% availability milestone in 2021, further investment is necessary to boost the quality and reliability of 4G service.

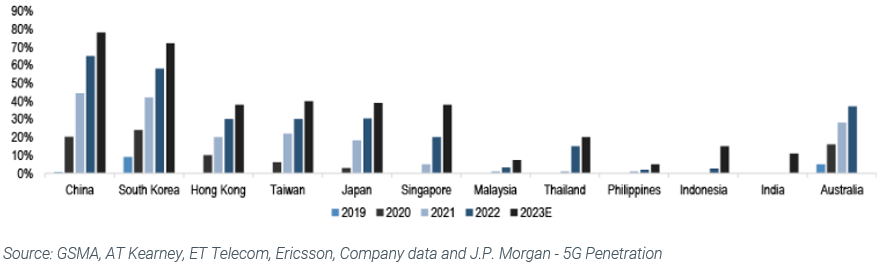

APAC markets are in various stages of 5G adoption across the spectrum, but Indonesia has yet to start its rollout. The success of 5G implementation and update depends on several factors, including policy, frequency spectrum, business models, infrastructure, and software. The roadmap for 5G implementation remains unclear because the country has yet to set a timetable for the auction of 5G spectrum to mobile carriers or decide which frequency the technology will operate. A new Cabinet is set to be installed in October 2024, which could drive changes in government policy and action regarding 5G. This development could lead to the commencement of 5G spectrum auctions towards the end of 2024 or in early 2025.

The TowerCo’s are extremely optimistic in monetising the future 5G-led capex cycle by the MNO’s. TowerCo’s are integral to 5G rollout, as the technology demands network upgrades and increased densification. This densification is achieved through backhauling, as well as distributed antenna systems (DAS) and small cells, which help to augment and strengthen network capacity. For TowerCo’s, this creates new opportunities for incremental tower builds and increased tenancies on existing tower sites.

Mitratel (MTEL) is best positioned among Indonesia’s TowerCos to capitalise on these key investment themes. It enjoys a strategic advantage due to its strong affiliation with its sister company Telkomsel, Indonesia's largest MNO, an extensive and underutilised tower portfolio traversing the entire country, the lowest exposure to the IOH rationalisation, the most developed ex-Java portfolio where MNOs are actively looking to expand, and the strongest balance sheet metrics within the sector.

China tower

In China, new tower growth for China Tower Corporation (CTC) has moderated from historic levels of 4-8% to about 1-2%. In 2023, the company experienced a brief boost as it cleared backorders, having faced disruptions in tower construction due to pandemic lockdowns in previous years. Looking ahead, this slowdown in growth appears structural, with mobile network operators (MNOs) emphasizing greater network sharing and cost optimization. The MNOs have indicated that 5G capital expenditures have peaked. We believe tower growth is unlikely to accelerate until the 6G investment cycle begins, which likely 2028-2030 at earliest.

We expect tenancy growth and pricing to support stable growth within the core tower business. The company's ‘Two Wings’ business, focusing on Distributed Antenna System (DAS) business and innovative energy services on one wing and Trans-Sector Site Application and Information (TSSAI) business on the other, is exhibiting double-digit earnings growth. This growth comes from increased revenue per customer, new customer acquisitions, and an expanded range of services. However, despite its rapid growth, we view the impact as minimal given these segments combined contribute less than 20% to CTC's total revenue.

CTC is fundamentally undervalued however we view it as a capital-trap. Despite a robust balance sheet and a strong free cash flow profile, the company's ability to increase distributions is limited by State-Owned Enterprise (SOE) rules, which prohibit dividend per share from exceeding earnings per share. Additionally, with only about 26% of shares publicly traded, share buybacks are restricted by listing rules requiring a minimum 25% free float. There is limited foreign investor appetite with all three of the company’s major shareholders and MNOs (China Mobile, China Unicom and China Telecom) on the United States’s trading ban.

Although based on pure mathematical calculation, 2026 could see a material step-up in net profit (and consequently dividend) due to savings from fully depreciated tower assets acquired in 2015. Management note that the actual step-up would also depend on continued investment in tower augmentation and replacement, which prolongs actual useful life of old towers leading to higher depreciation costs and offsetting any expected gains in net profit.

Portfolio positions

Despite ongoing political and economic headwinds across the globe, this trip sees us reaffirm our investment in the Asian region. We have factored in the risk and believe the value proposition of the quality infrastructure names continue to be very attractive.

In summary

- Airports: Asia is back after a slower start to the post COVID rebound. Both in-bound, out-bound and domestic traffic momentum remains buoyant supporting both economics and infrastructure names. In particular we like the airports in Malaysia (fundamental growth and special situation) and airports of Thailand (the return of the tourist)

- Toll roads: The rise of the middle class remains a core theme across the region, and we believe toll roads are a fantastic way to capitalise on this evolution – both passenger and heavy vehicle travel momentum supported by a growing middle class and improving economic outlook. Further, the opportunity for more growth in the sector provides upside support – roads are core to economic evolution. We favour Indonesian toll road operator Jasa Marga and the Chinese operators exposed to the relatively resilient Tier 1 cities such as Shenzhen International.

- Energy: A growing middle class coupled with a global desire for a greener future makes for a huge investment opportunity across the region. However, as investors we seek not only growth but reliable returns which limits the current regional investment universe linked to this theme. We welcome improved regulation in the Chinese gas sector reaffirming our investment in the space, while waiting for improved regulatory visibility in other areas before considering investment.

- Communications: Not all tower companies are created equal. While the opportunity set of 5G and data is universal, the framework and ability to execute is disparate. Within the Asian space we favour Mitratel in Indonesia who has the geographic footprint, asset quality, balance sheet and strong management team to truly capitalise on the opportunity.

- Diversified: Unfortunately, the diversified players within our universe have a wide asset mix and varying headwinds/tailwinds. While we like the infrastructure assets within these names, the periphery businesses remain very mixed with some fundamentally value-destructive elements ruling out investment. The exception to this is Shenzhen International, a very high-quality player in the infrastructure space with non-infrastructure exposure limited to Tier 1 cities where demand is strong and value realisation very visible.

- Yield: While we like most investors like yield, more important to our investment decision is fundamental value, total return and quality. As such, while we have not downgraded names based on dividend decisions alone, we have downgraded them on quality as management fail to act in shareholder interest.

As always, we maintain a diversified portfolio of high-quality infrastructure names globally, and at the moment, believe parts of Asia are offering an attractive mix of quality and value.

[1] International Air Transport Association (IATA) 2023 report

[2] Dragon Trail International - Chinese Traveler Sentiment Report: April 2024

[3] https://www.oxfordeconomics.com/resource/chinese-outbound-travel-to-gain-momentum-in-2024/

[4] https://digital.theedgemalaysia.com/theedgemediagroup/pageflip/swipe/tem/20240226tem#/10/

[5] Dollar margin represents the gross profit per unit of gas sold. It is calculated as the difference between the cost of purchasing the natural gas and the revenue gained from selling it at the city-gate.

The content contained in this article represents the opinions of the author/s. The author/s may hold either long or short positions in securities of various companies discussed in the article. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the author/s to express their personal views on investing and for the entertainment of the reader.