This article is a follow up to our November 2024 News & Views “Tariffs: The impact on Infrastructure”. The last two weeks have broken multi decade records for intraday equity market reversals and single day rallies. We have also seen heightened bond market volatility, a material repricing of US and global growth and inflation expectations, and increased Fed rate cuts priced in for 2025. Geopolitically, Trump has aggressively started to isolate America, while also maintaining attacks on China as a trading partner, effectively leading to a cutting of the majority of China - US two-way trade.

In this article, we will review the recent tariff developments and where we stand today, the potential impacts on the US and global economies, and consider the impact on global listed infrastructure sectors and stocks.

Background – Trump’s first two months in the White House

Tariffs and immigration were two cornerstone policies of Trump’s 2024 election campaign. Over Q1 2025, federal government policy ambiguity has been increasing as Trump postulated on tariff implementation, as well as uncertainties brought on by the implementation of DOGE cuts and immigration curbs. There was some optimism in February and March when Trump backpedalled on 25% Mexico and Canada tariffs with a one-month delay, and then carved out USMCA compliant goods, while he held firm on additional China tariffs, Auto tariffs and 25% Steel & Aluminium tariffs.

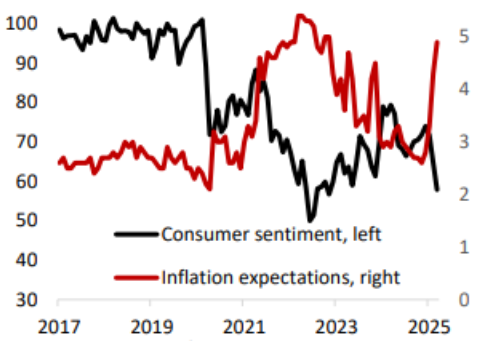

At the same time, US economic growth started to deteriorate, with retail sales and personal spending surprising to the downside, and weakness in sentiment with consumer and business confidence surveys losing traction. US consumer sentiment hit a 2 ½ year low in March, and consumer inflation expectations hit the highest since 1993 (five year horizon inflation at 3.9%).

Source – University of Michigan, DBS

So far, the labour market remains strong and corporate earnings have held up - in contrast to soft survey data. However, cost pressures have been increasing, seen in the S&P Global PMI in January and February, which leaves the Fed in a difficult situation of a weakening economy but elevated, and potentially increasing, inflation outlook. Manufacturing activity data, seen in the US ISM PMIs, slowed to contractionary levels in March, with an even greater deterioration in forward looking new orders. This suggests the uptick in manufacturing in January and February, to the highest in 27 months, was just a pull-forward of demand ahead of anticipated Trump tariffs and not a sustained pickup in industrial activity.

This economic deterioration in the US led the market to question the resounding ‘US exceptionalism’ thematic that has been in play since Covid, with a particular focus back to Europe. In the first quarter, the S&P 500 fell 2%, with a 7% drawdown from February highs while Europe rallied 7%. This shift was further fuelled by Trump’s undermining of the NATO alliance, which saw European leaders galvanised into a level of unity not seen in decades. This led to expansionary fiscal stimulus including defence spending at the EU level, a €500b German infrastructure and defence fund, and loosening of strict government fiscal restraints.

Obliteration Day

All these Q1 developments were the precursor to the main action of 2025: April 2, Trump’s so-called ‘Liberation Day’, which turned out to be ‘Obliteration Day’. This was the grand reveal of Trump’s tariff plan globally, after an extensive US Trade Representative (USTR) review of global tariff policy.

“This is the beginning of Liberation Day in America. We’re going to charge countries for doing business in our country and taking our jobs, taking our wealth, taking a lot of things that they’ve been taking over the years. They’ve taken so much out of our country, friend and foe. And, frankly, friend has been oftentimes much worse than foe.”

President Trump, leading up to April 2

In the weeks preceding ‘Liberation Day’, Trump flagged a 10% Universal Base Tariff, as well as hints around potential reciprocal tariffs – charging the same tariffs as other countries were charging the US. On April 2 Trump announced a national emergency to “increase the nation’s competitive edge, protect our sovereignty, and strengthen our national and economic security”, which enabled him to invoke the International Emergency Economic Powers Act (IEEPA) and enable him to issue an Executive Order on tariffs.

The announced tariffs were far more aggressive than most bear cases, with a 10% Universal Base Tariff (as expected), very high reciprocal tariffs on 27 countries and the EU bloc, as well as ending De Minimis exemptions (which allow duty free goods entry under $800 USD, typically from China and Hong Kong). To their great relief, Canada and Mexico were left off the reciprocal tariff list.

Country level Liberation Day Tariffs

Source – DBS, White House

Bloomberg estimated that the new effective US tariff rate would be 22%, 10 times higher than currently, and the highest since the early 1900s. Trump also left the door open to even higher (or lower) rates with “modification authority”, as well as excluding certain sectors by flagging additional sector-based tariffs to be announced imminently (pharmaceuticals, semiconductors, gold, lumber, copper). Several countries received the minimum reciprocal tariff of 10% including Brazil, UK, Singapore, Australia and New Zealand – as well as some inhabited by mere penguins and seals (Heard and McDonald Islands). The Nomura Research Institute [1] noted:

“After World War II, the United States championed the promotion of free trade to prevent a repeat of past mistakes. However, the Trump administration is now significantly shifting this policy, threatening to dismantle the global free trade system. This shift will likely reduce economic efficiency and slow global growth.”

Cumulative change in US average tariff

Source – NAB

The very hawkish tariffs, both in size and breadth, surprised the markets. There were no carve outs for companies or sectors that had given investment pledges to the US, nor was it certain that any negotiations would occur considering the short time frame till tariffs went live (under a week). The S&P500 and Nasdaq fell over 10% in the following days. Bond yields, after initially falling to below 4%, rallied aggressively with US ten year bonds hitting 4.5%, the steepest two day move in yields in two years. The increase in longer term yields, while shorter term yields stayed low with the expectations of more Fed cuts, was what was most troubling to the market – a repricing of the US term premium, with the market demanding a higher premium for the level of economic uncertainty, large fiscal debt and deficits long term. This was even more pronounced in an ever-isolating posturing by the US, potentially impacting demand for the USD and the ability to continue funding large deficits, which are funded substantially from foreign investors.

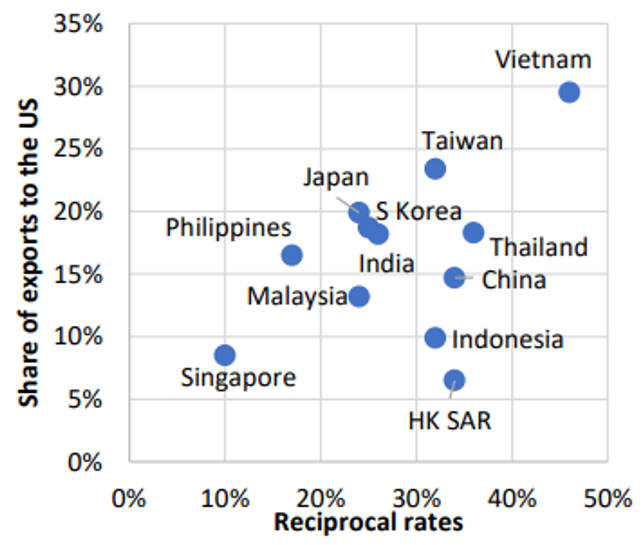

Vulnerabilities from proposed reciprocal tariffs

Source – DBS, CEIC

The level of retaliatory tariffs from other countries are expected to have a major impact on US trade flows, growth and inflation. China, whacked with a 34% tariff, retaliated with a 34% tariff. Trump then added another 50% tariff (to 84%) on Tuesday 8 April which China matched, encouraging Trump to go even harder and imposing a 125% tariff by Wednesday April 9. This took overall China tariffs to 145% since coming into office in January 2025. The reality is 84% versus 145% is quite irrelevant given trade between the two countries is likely to cease under either scenario. The Chinese finance minister indicated that it would ignore any further tariff increases from US on China-made goods stating that given there is "no longer possibility of market acceptance" for US goods to be exported to China, it will pay no attention to it”.

For reasons known only to himself, on April 9 Trump announced a 90 day pause on all reciprocal tariffs except for China, while maintaining the 10% UBT tariffs and sector tariffs. While this led to a large relief rally - the biggest single up move since 2008 in US equities - risks remain. The global economy, and the US, are not out of the woods yet. There remain many unknowns, economically and geopolitically, with both short and long term impacts. In particular:

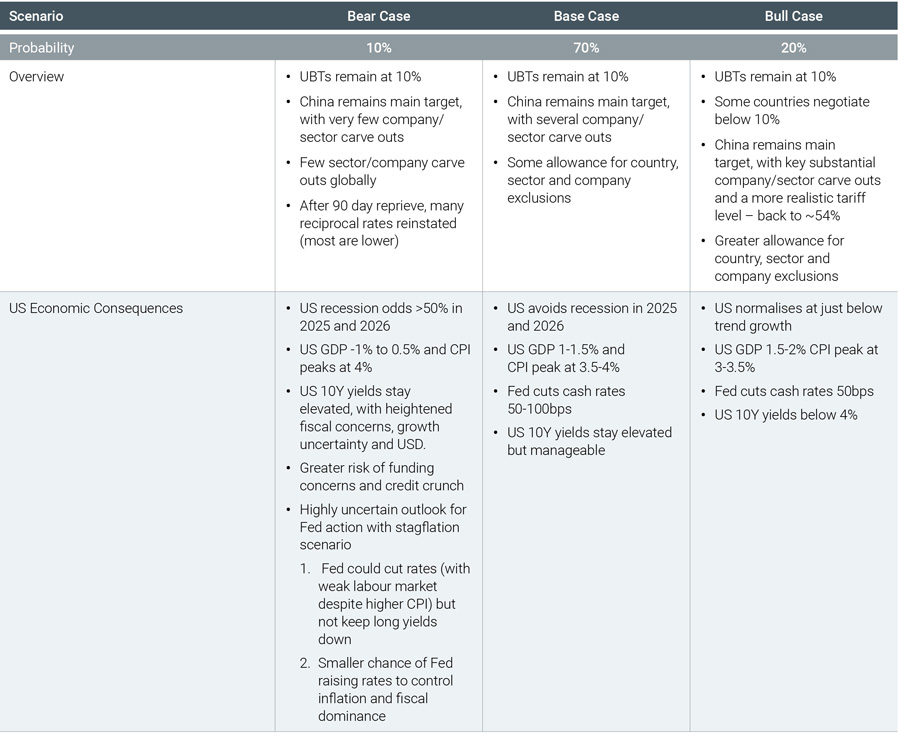

The macroeconomic impact of tariffs on countries – Scenarios

In our November 2024 News & Views “Tariffs: The impact on Infrastructure”, we stated “On their own, tariffs are broadly negative for US growth, boost inflation and put the Fed on hold (or on a slower path down).” The Liberation Day announcement led to much more aggressive downgrades of US growth, upgrades to US CPI and a bring-forward of Fed cuts.

- The market moved from two cuts in 2025, to five for the Fed – which would grapple with managing its dual mandate just as CPI increases and the outlook for the labour market (and growth) weakens.

- Most investment banks cut GDP forecasts to 1-2% for 2025-6 and added 2% to US CPI to 3.5-4% levels. The increase in inflation would hit household income and consumption, which would have a larger impact than any potential Trump tax cuts.

- US recession odds, priced by the market and forecasters, increased to 40-50%. Key transmission channels in the economy from the tariffs are household consumption (lower real disposable income), and lower business sentiment (lower capex and hiring).

Of course, post Trump’s 90 day pause of reciprocal tariffs, a lot of these worse case downgrades may be pared back as Trump steps away from the brink. However, we broadly see three scenarios of tariff outcomes and their respective impact on macroeconomic outlook.

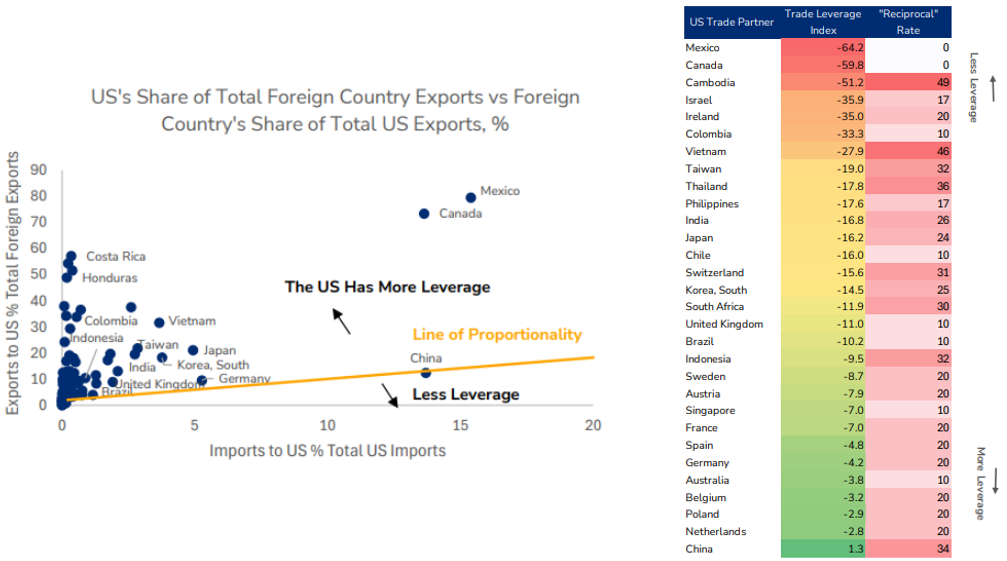

The impacts on regional economies are highly dependent on upcoming negotiations. However, we do know that certain economies are more hamstrung based on structural elements of their economy and import/export mix, while others have a greater ability to threaten (or impose) retaliatory tariffs. This includes those countries with a low export mix to the US and a low % of GDP, as well as those with immaterial US imports. China and Europe have the most leverage to fight back, according to the Wolfe Leverage index.

Wolfe Leverage Index – Who has the most leverage to fight back?

Source – Wolfe Research

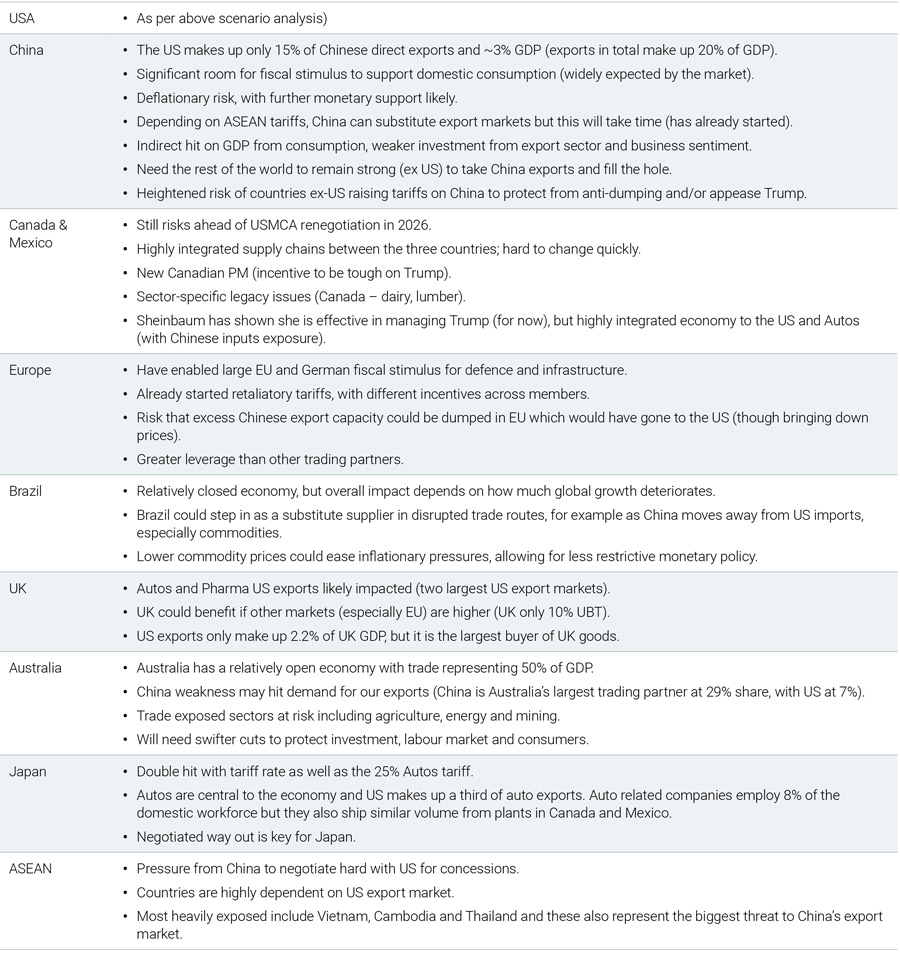

A brief summary of main impacts of tariffs across the globe:

In addition to the uncertainty brought on by the 90 day pause and where tariffs may settle, there are also longer term and structural impacts that must be considered, namely:

- There will be a complete re organisation of global supply chains between US and China, and a trend away from the US regardless of the scenario that eventuates (ie an ‘isolated America’). New capacities built onshore can only service onshore demand.

- Risk of loss of confidence in the US Dollar and less demand for US treasuries, which may impact capital flows and funding their fiscal deficit.

Impact on global listed infrastructure

Infrastructure has characteristics which support long term visible and resilient earnings streams. These characteristics should prove attractive relative to broader equities in very uncertain economic and geopolitical environments. Further, infrastructure is quite unique in that within our universe, we have macro diversity as well as regional diversity. As such we can actively position a portfolio with consideration of in-country macro drivers to fundamentally weather the evolving economic and geopolitical environment. That is not to say however, that this environment poses no threat to the asset class. In our November 2024 News & Views “Tariffs: The impact on Infrastructure”, we stated:

“Infrastructure stands at the crossroad of global trade – ports allow for the movements of goods across the seas, while goods are moved from ports to demand centres by railway and road infrastructure. Tariffs also have a potential impact on countries’ growth and inflation outlook, which impacts the macroeconomic variables driving infrastructure’s long-term return outlook.”

Trump’s Liberation Day announcements were detrimental to pretty much every segment of the market, including infrastructure, with few absolute winners within our universe. On a relative basis, we expected infrastructure to be more resilient but the economic consequences would have been felt. Thankfully, by implementing a 90 day pause and indicating a willingness to negotiate directly with countries, it would appear Trump has stepped back from the most extreme action, increasing the likelihood of our base case (above) eventuating, a clear improvement on the Liberation Day worst case outcome (bear case above).

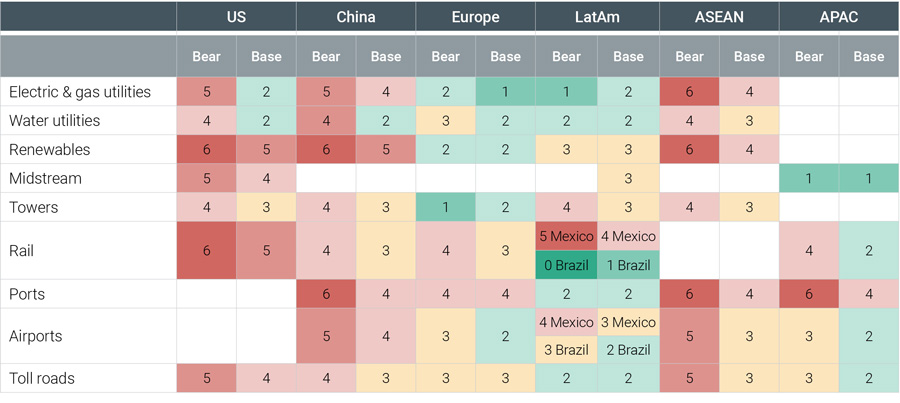

Relative impact per infrastructure sector

The impact to infrastructure is very nuanced and we will publish detailed analysis on each sector in a later piece. However, in summary, the relative attractiveness of sectors/regions within the infrastructure universe are summarised below for our base case and again for the bear case – should the situation deteriorate.

Relative exposure (red) versus relative protection (green) within the listed infrastructure universe

Source: 4D Infrastructure

Broadly speaking a deterioration of our base case to the bear case would lead to more pronounced negative outcomes among key sectors including:

- US: Rail is impacted the most (with intermodal the most directly linked to trade and weaker domestic consumption), while Renewables are impacted by offshore supply chains and uncertainty over IRA repeals. Utilities are impacted by some pull back in growth expectations (AI upside), but generally should have resilient earnings even in recessions. However, the Fed quandary of cuts versus hikes, and the steepening of the yield curve, puts Utilities and Renewables most at risk.

- China: Ports are most heavily impacted (changing trade patterns), particularly as related to the ASEAN relationship, while Airports will be impacted by an international spending slowdown. The level of fiscal support should offset some impact on overall GDP sensitive sectors, such as Toll Roads, while Electric & Gas utilities with the highest industrial exposure will feel the greatest impact.

- UK/Europe: Impacted to a lesser extent, with the internationally exposed businesses hit most but still relatively better off than the US and China (ie international passengers at airports, offshore renewable investment plans). Also, could benefit from a reallocation of trade.

- LatAm: Brazil and Mexico very different players in these trade wars. Brazilian toll roads, rail and port companies exposed to potentially higher commodity demand from China could benefit while those airports that are predominantly domestic traffic are more protected. Brazilian utilities could also benefit from a shift in data centre demand onshore given issues facing the US. By contrast, Mexican rail is highly exposed while the airports are fragmented based on relative exposure to US versus domestic passengers/cargo, exposure to Mexican onshoring and associated FX implications.

It should also be noted that we believe a negative infrastructure outlook should still be relatively better than many sectors in the market, where earnings are not underpinned by the key characteristics that makes infrastructure resilient (monopolistic, contracted or regulated, inflation hedged).

Conclusion

In our 2025 Outlook piece we commented that predicting Trump’s every move was “a fool’s game”. Sadly, that has proven to be true with recent actions creating significant market and macro uncertainty. Unfortunately, we see no great clarity over Q2 with Trump’s actions highly unpredictable.

Fundamentally, infrastructure earnings should hold up relatively well, however, we recognise that there are many near term sector nuances. In this piece we have tried to articulate the high level risks and opportunities across the globe at a macro level and the relative attractiveness of sectors/regions within our infrastructure universe.

While the situation remains very fluid, our recent analysis supports our current overweights to Europe and parts of Latin America and an increased appreciation of defensive sectors with strong yields. We will continue to monitor the global macro, regional and sector impacts and position the portfolio accordingly within the highly diverse infrastructure universe.

1. https://www.nri.com/en/media/column/nri_finsights/20250403.html

The content contained in this article represents the opinions of the authors. This commentary in no way constitutes a solicitation of business or investment advice. It is intended solely as an avenue for the authors to express their personal views on investing and for the entertainment of the reader.